National Insurance contributions (NIC’s) have increased as of the 6th of April 2022. The increase was announced in the Budget of October 2021.

The increase of 1.25% in NIC’s will affect both employers and employees.

The amount of NIC’s you pay as an employee depends on your national insurance category letter and how much of your earnings fall within each NI band. In the tax year 2022/23 the categories and bands are shown as follows:

National Insurance Categories

| NI Category | Employee Group |

| A | All employees apart from those in groups B, C, H, J, M, V and Z in this table |

| B | Married women and widows entitled to pay reduced National Insurance |

| C | Employees over the State Pension age |

| H | Apprentices under 25 |

| J | Employees who can defer National Insurance because they are already paying it in another job |

| M | Employees under 21 |

| V | Employees who are working in their first job since leaving the armed forces (veterans) |

| X | Employers use category letter X for employees who do not have to pay National Insurance, for example because they are under 16. |

| Z | Employees under 21 who can defer National Insurance because they are already paying it in another job |

National Insurance Bands & Rates

| NI Category Letter | £533 to £823 Month | £823.01 to £4,189 Month | Over £4,189 Month |

| A | 0% | 13.25% | 3.25% |

| B | 0% | 7.1% | 3.25% |

| C | N/A | N/A | N/A |

| F | 0% | 13.25% | 3.25% |

| H | 0% | 13.25% | 3.25% |

| I | 0% | 7.1% | 3.25% |

| J | 0% | 3.25% | 3.25% |

| L | 0% | 3.25% | 3.25% |

| M | 0% | 13.25% | 3.25% |

| S | N/A | N/A | N/A |

| V | 0% | 13.25% | 3.25% |

| Z | 0% | 3.25% | 3.25% |

National Insurance Class

In addition to national insurance category letters and bands, we also have national insurance classes, which are shown in the table below.

| NI Class | Who Pays |

| Class 1 | Employees earning more than £190 a week and under State Pension age – they are automatically deducted by your employer |

| Class 1A or 1B | Employers pay these directly on their employee’s expenses or benefits |

| Class 2 | Self-employed people earning profits of £6,725 or more a year. If you are earning less than this, you can choose to pay voluntary contributions to fill or avoid gaps in your National Insurance record |

| Class 3 | Voluntary contributions – you can pay them to fill or avoid gaps in your National Insurance record |

| Class 4 | Self-employed people earning profits of £9,881 or more a year |

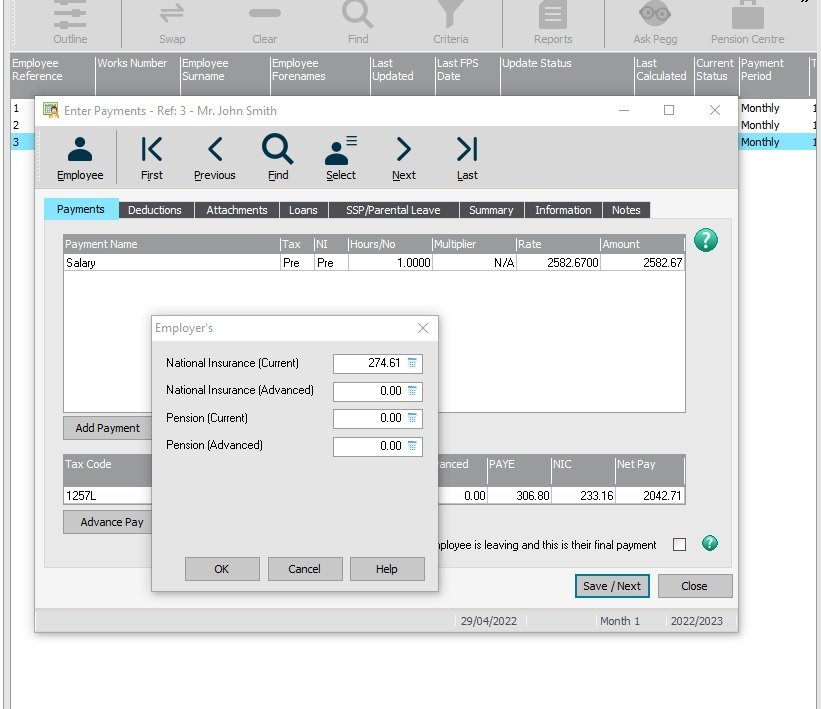

Assuming you are an employee with a standard rate contribution NI category letter of A, and earning the average UK annual salary of £30,992 (ONS Average Weekly Earnings 03/2022) your Class 1 NIC’s per month would be £233.16 calculated as follows:

£823.00 X 0% + (£2,582.67 – £823.00) X 13.25% = £233.16

Your employer would pay £274.61 in Employers NIC’s.

Employers NIC’s

NIC’s for employers, also known as Secondary Class 1 contributions, have risen from 13.8% to 15.05%. for earnings over £175.00 per week subject to the NI category for each employee.

Employees NIC’s

NIC’s for employees, also known as Primary Class 1 contributions, have risen from 12% to 13.25% for earnings over £190 per week. Earnings above £976 a week for employees have risen from 2% to 3.25%.

You will need to check the NIC’s category letter that applies to you and your circumstances. For example, category B applies to married women and widows entitled to pay reduced NIC’s.

Sage Payroll

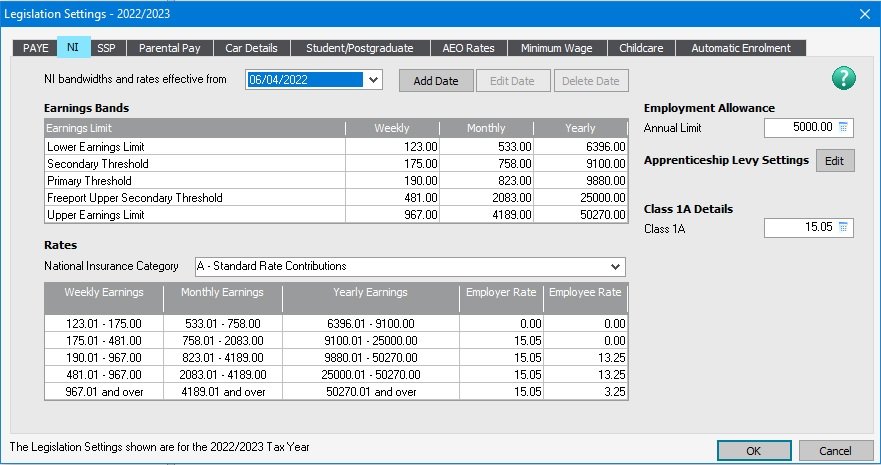

As we process all our payroll via Sage Payroll software all these updates are taken care of with regular updates of the software. Checking for legislation changes for the software is an automatic part of processing payroll.

As you can see in the image below, all legislation settings and parameters are in the payroll software and updated as required. That includes everything from PAYE and NI to Minimum Wage and Auto Enrolment.

Self-Employed NIC’s

Self-employed NIC’s on profits above £6,515 a year, also known as Class 2 contributions, have risen from £3.05 a week to £3.15. Class 4 contributions payable on self-employed profits above £9,568 have also increased from 9% to 10.25% and Class 4 NIC’s on self-employed profits above £50,270 have increased from 2% to 3.25%.

Company Directors Dividend Tax

For company directors taking a dividend payment, the dividend tax rate for basic rate taxpayers has increased from 7.5% to 8.75% and for higher rate taxpayers from 32.5% to 33.75%.

PAYE & NI Confusion?

In my experience tax codes and tax code changes cause the most concern for employees in relation to their pay calculations. In relation to the self-employed, its Class 2, Class 3, and Class 4 NIC’s.

The best solution to ensuring you have a pain free payroll is:

- Use a reliable and trustworthy payroll software, like Sage 50Cloud Payroll www.sage.co.uk

- Make sure your payroll provider has the necessary payroll skills Sage Certified Expert